London Flexible Office Space Report - Q2 2025

Rubberdesk's Flexible Office Space Report examines actual flex office availability and pricing as well as trends in London.

Our Flexible Office Space Market Report for London provides an insider's view of the current supply and pricing of the Greater London coworking and flexible office market.

London's Flex Market Defies Headwinds as Demand Drives Continued Growth

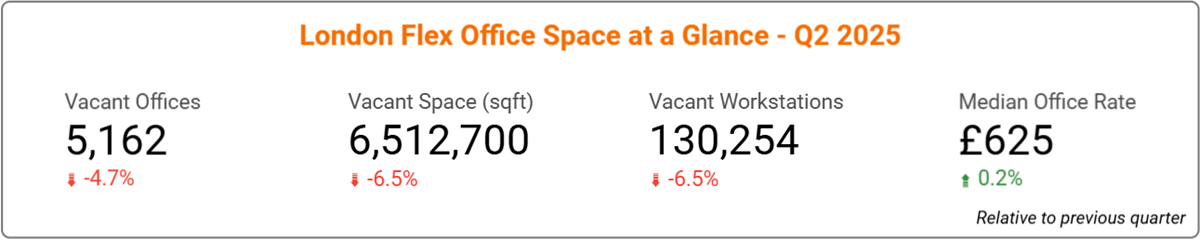

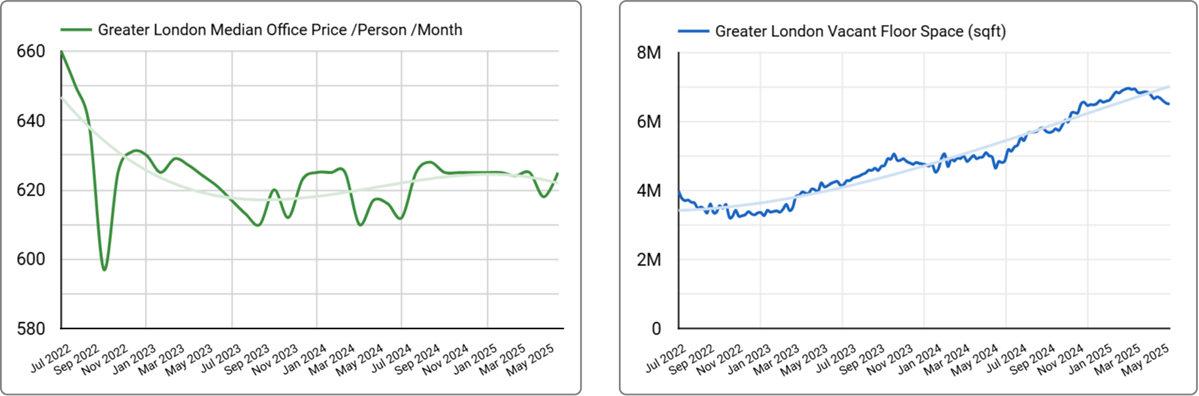

London's flexible office market remained strong in Q2 2025, with average desk rates holding steady at £625 per desk (+0.2% quarterly increase) despite overall available space contracting by 6.5% to 6.5 million sq ft through strong occupancy.

A Flex Market in Flux

The defining trend continues to be Managed offices' exceptional growth, expanding 1.9% quarterly to reach 2.9 million sq ft and with year-on-year growth 101%. The rise of Managed offices suggests that traditional landlords are fundamentally restructuring portfolios to meet what appears to be permanent business demand for flexible term with low capital outlay for all inclusive, turnkey fitted space.

"We're witnessing a fundamental shift in how commercial office space is being packaged and marketed," said Jim Groves, CEO. "As high vacancy rates and hybrid work models persist, landlords have strategically pivoted to provide flexible agreements to meet evolving market demands."

Regional Market Impact

Central London's 4.8 million sq ft declined (-7.8% quarterly) while rates remained stable at £700. Strong performance outside Central London appears to have driven desk rates higher in West London (+5.6% to £475) and North London (+5.1% to £394) as businesses potentially seek more affordable options outside the city centre.

Rates in East London increased (+2.7% to £485), likely influenced by a higher proportion of managed offices entering the market while overall availability fell marginally (-0.8% to 827,600 sq ft). South London saw available space fall (-5.3%) with competitive positioning at £320, suggesting healthy market dynamics across all London submarkets.

Source: Rubberdesk August 15, 2025

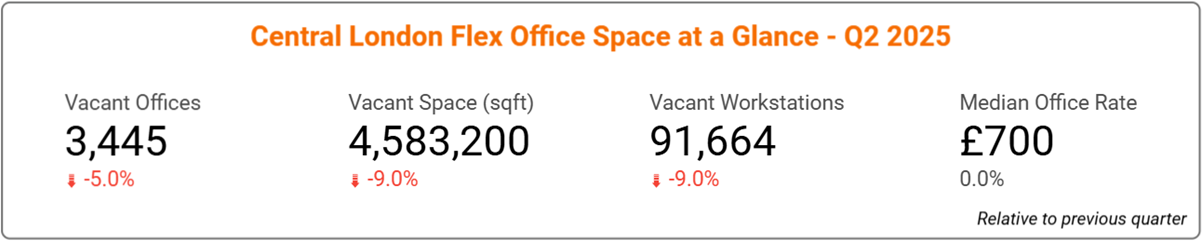

Strong Occupancy Drives Space Contraction Across Central London Districts

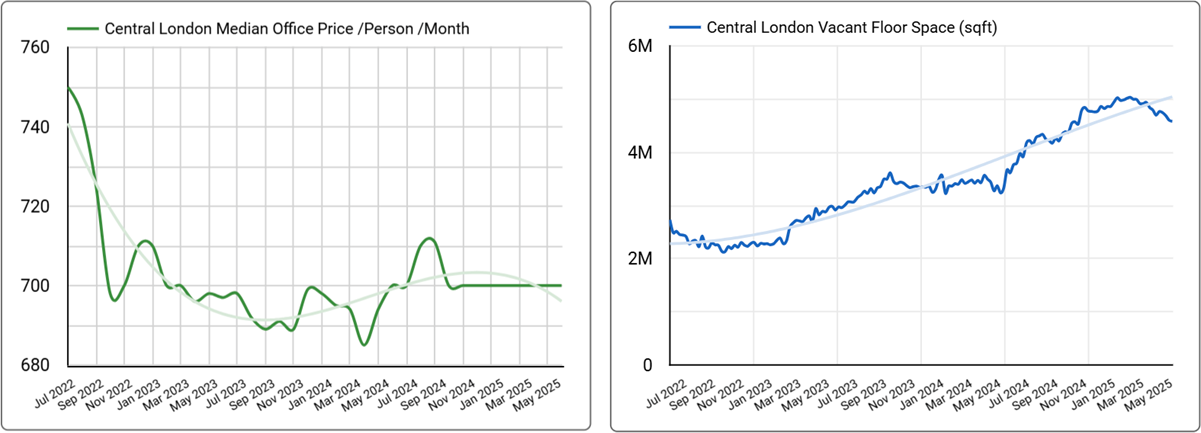

Desk rates in Central London held steady at £700 per desk while available space contracted by 9.0% to 4.6 million sq ft through strong occupancy across the capital's core business districts.

The defining trend continues to be the divergence between office types. Managed offices grew 2.6% quarterly to reach 2.1 million sq ft despite a broader drop in availability, with year-on-year growth reaching an extraordinary 125%. This expansion likely reflects permanent business demand for customized flexible solutions. Managed office rates at £850 showed resilience, declining modestly (-2.0% quarterly) while maintaining positive annual growth (+3.0%).

The Serviced office sector reflected what appears to be healthy market take-up, with available space declining 14% quarterly to 2.5 million sq ft as businesses seemingly migrate from traditional arrangements to professional workspace. Rates at £665 (-0.7% quarterly) offer considerable value for cost-conscious businesses.

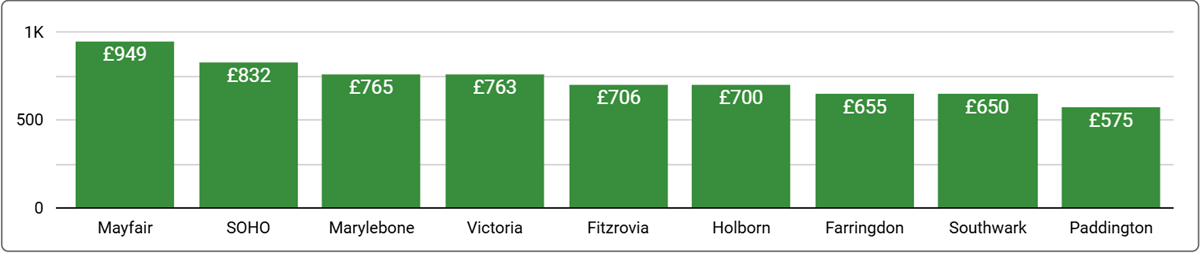

The market now offers compelling affordability contrasts across key areas. Premium locations command top rates, with Mayfair at £949 despite recent moderation (-4.6%), SOHO at £832 (+1.1% quarterly), and Marylebone at £765. Meanwhile, value-focused businesses can access quality flexible space in Holborn at £700 (+0.6%), Southwark at £650 (+1.1%), and particularly Paddington at £575 following a significant reduction (-19%) in desk rates. This pricing diversity provides businesses considerable choice between prestige locations and cost-effective alternatives.

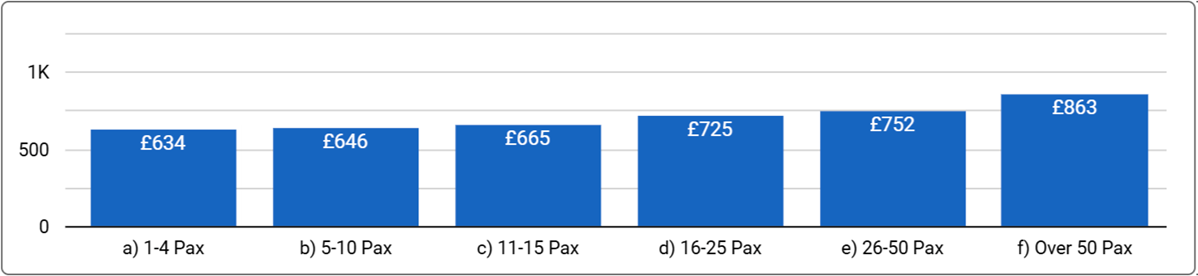

Team size preferences revealed mid-market resilience, with 26-50 person segments showing rate growth (+1.1% quarterly to £750), while larger office requirements experienced saw prices dip (-2.6% quarterly to £854), due to the sheer amount of new supply across this segment.

"Landlords are now shaping the demand, not just reacting to it. The rise of managed offices shows how quickly the market is pivoting to meet the needs of modern businesses.”

Tom Petryshen, VP Growth & Analytics

Source: Rubberdesk August 15, 2025

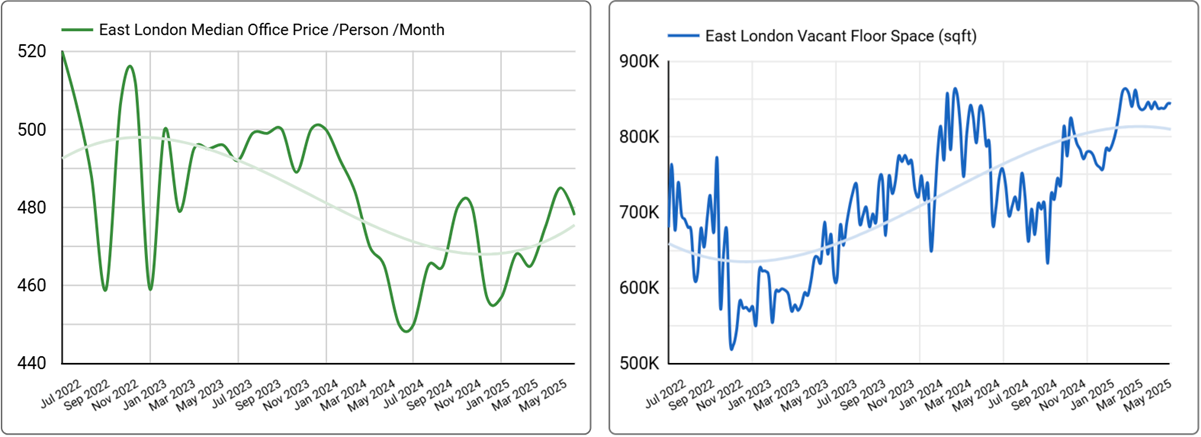

Strong Demand Drives East London Flexible Office Rates Higher

London's second-largest flexible office region showed strong momentum in Q2 2025, with desk rates rising 2.8% quarterly to £478 while available space declined 1.5% to 844,200 sq ft, suggesting healthy demand across this strategically positioned area.

Managed offices drove the region's performance, with space growing 13.5% quarterly to 482,500 sq ft while rates increased 9.6% to £685. The remarkable 35% annual growth in rates likely reflects both strong business interest in tailored solutions and the increasing proportion of higher-priced customizable options within the market mix.

Serviced offices, which are typically smaller than Managed office options, maintained stable rates at £445 while space contracted 16.9% quarterly to 355,700 sq ft, suggesting strong take-up as businesses apparently embrace professional workspace over home-working arrangements.

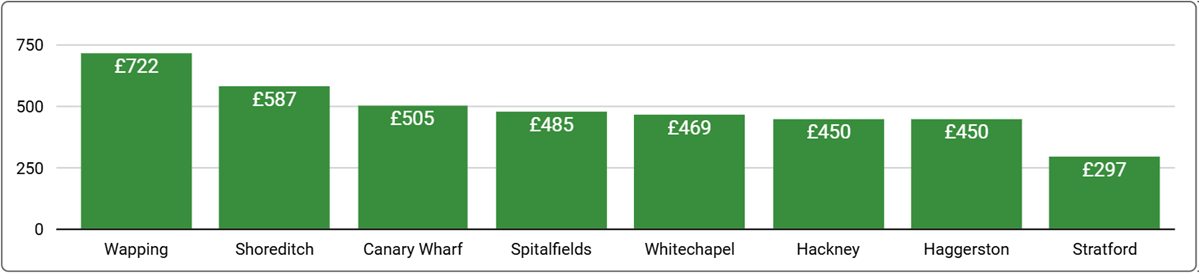

With direct access via the Elizabeth tube line, Canary Wharf emerged saw the largest rate increase climbing 12% quarterly to £505, providing premium building access at competitive rates. Hackney demonstrated strong momentum (+11% to £450), while Wapping maintained premium positioning at £722. Shoreditch, despite falling rates (-6.1% to £587), remains the region's largest district with nearly 190 offices.

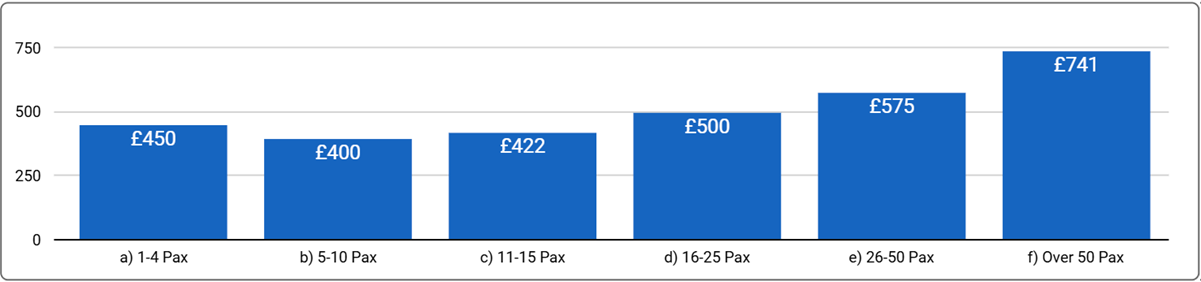

Across different office segments, mid-to-large offices showed particular strength. Spaces for 26-50 people saw rate growth (+4.5% quarterly to £575), while enterprise requirements (50+ people) remained stable at £741. The region's diverse pricing from £297 to £722 per desk ensures accessibility across various business scales and budget requirements.

Source: Rubberdesk August 15, 2025

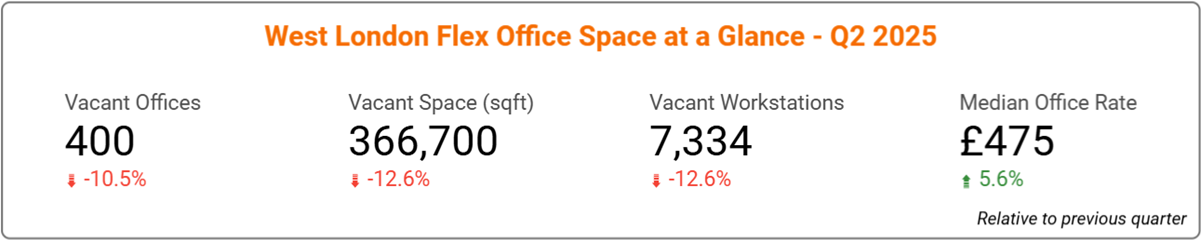

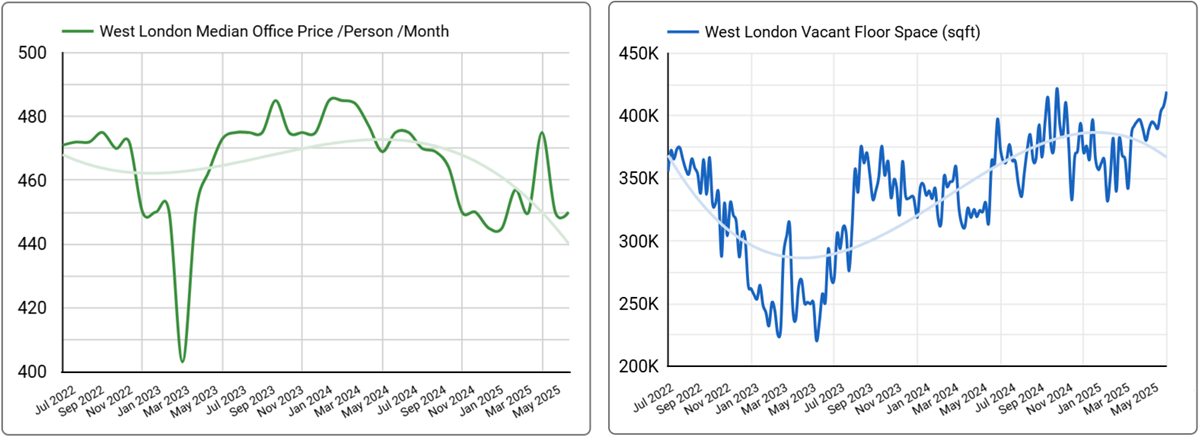

West London Rate Growth Accelerates as Space Tightens

West London achieved the strongest rate growth across London regions in Q2 2025, with desk rates rising 5.6% quarterly to £475 while available space fell 12.6% to 366,700 sq ft, suggesting strong occupancy across this strategically positioned region.

Both office types showed resilience, though with different trajectories. Serviced offices were popular, with rates rising 3.6% quarterly to £466 while space declined 11% to 298,100 sq ft. Managed offices though commanded premium positioning at £553 (+1.1% quarterly) despite space contracting 21%, potentially indicating strong corporate interest in tailored environments.

Hammersmith lead this segment of the market with rates rising 0.9% to £537 while space remained relatively stable across 102 offices. Kensington & Chelsea saw rates rise 13% to £425, supported by a 189% annual increase in available space as new supply enters this premium market. Fulham showed rate resilience (+3.8% to £519) despite availability falling.

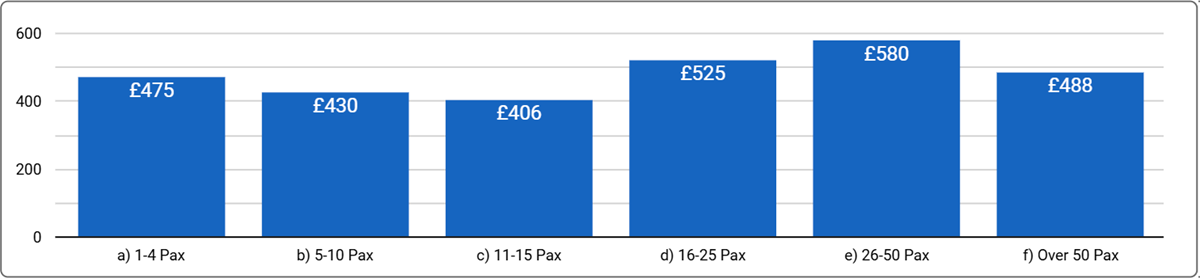

Offices for smaller team experienced notable rate increases, with spaces for 11-15 people rising 16% to £406 and 5-10 person offices climbing 11% to £430. This suggests strong demand for flexible solutions that may accommodate hybrid working models across West London's diverse commercial landscape.

Source: Rubberdesk August 15, 2025

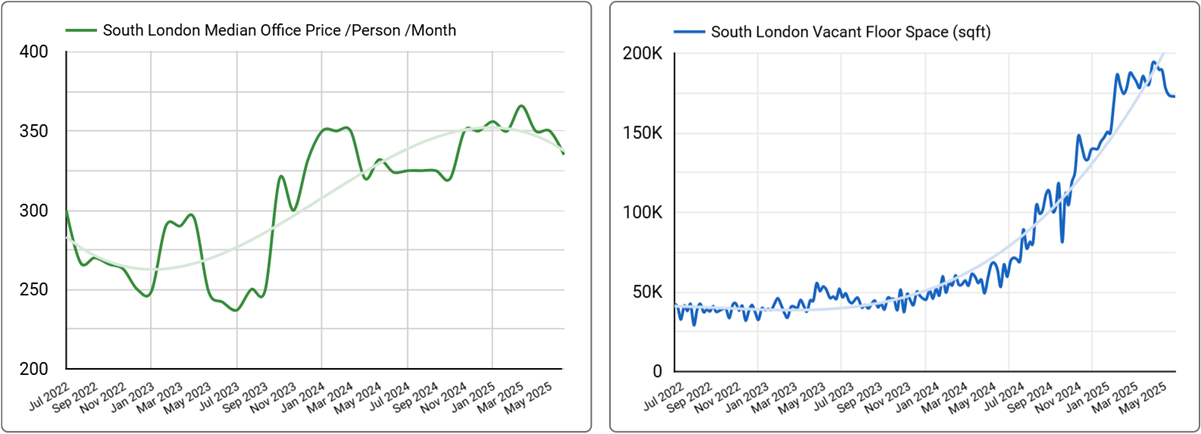

South London Market Adjusts as Supply Expands Considerably

Rate corrections dominated South London's flexible office landscape in Q2 2025, with desk rates declining 8.5% quarterly to £335 while available space contracted 6.6% to 173,000 sq ft. However, the remarkable 190.3% annual space expansion suggests the region's potentially rapid emergence as a major flexible office destination.

Rate pressures affected both workspace segments, albeit differently. Serviced offices experienced rate pressure with rates falling 12% quarterly to £317, while space contracted 12% to 133,350 sq ft. Customizable managed offices maintained premium positioning at £438 despite rate moderation (-4.6% quarterly), with space expanding 22%. The extraordinary 1430% annual growth in customizable space likely reflects major landlord investment in this emerging segment, though such dramatic growth figures warrant careful interpretation given potential data variations.

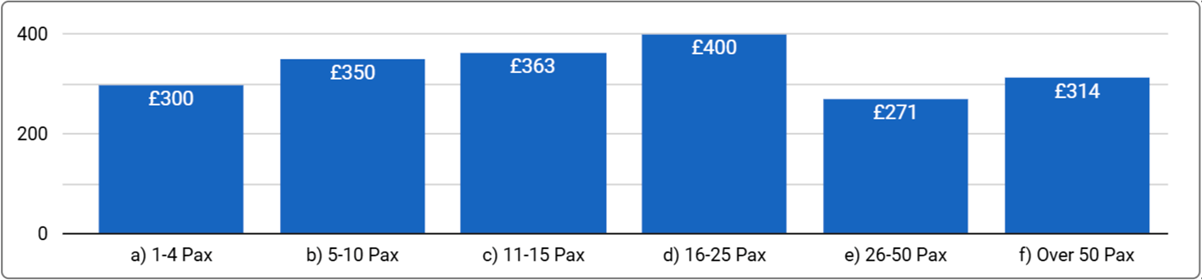

Enterprise and mid-market segment offered excellent value. Mid-market requirements (16-25 people) showed substantial annual space growth at competitive £383 rates, while enterprise solutions (50+ people) demonstrated exceptional expansion at £314 per desk. This positions South London as increasingly attractive for businesses seeking professional workspace at competitive rates, though businesses should consider market volatility when making location decisions.

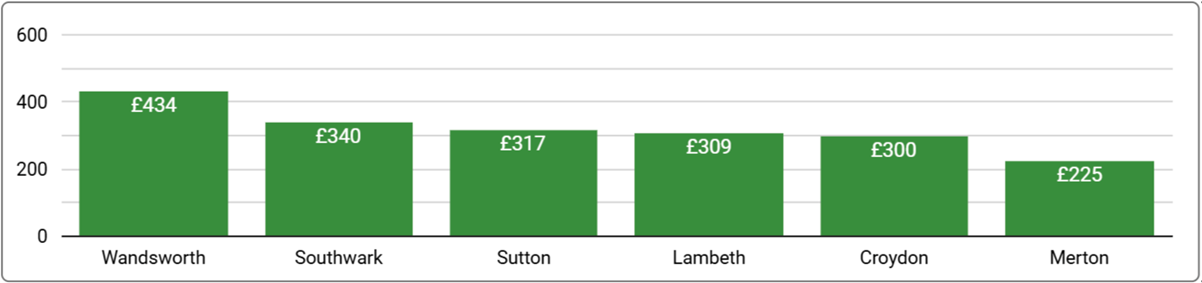

Wandsworth demonstrated resilience with rates rising 4.8% quarterly to £434 across 71 offices while Southwark offered considerable value at £340 per desk with exceptional annual space expansion, potentially establishing it as a major flexible office hub. Lambeth provided cost-effective solutions at £309 (+3.0% quarterly) with robust annual growth, while Croydon remained competitive at £300.

Source: Rubberdesk August 15, 2025

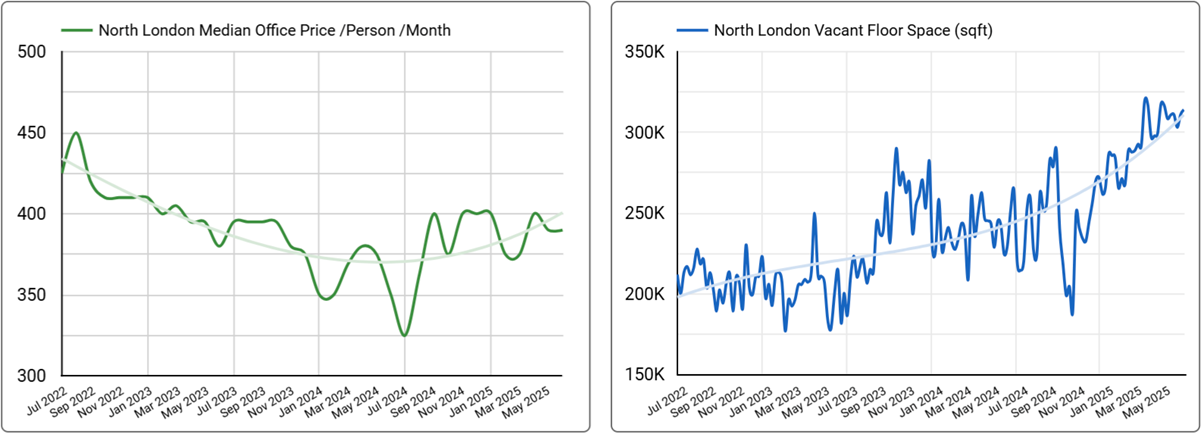

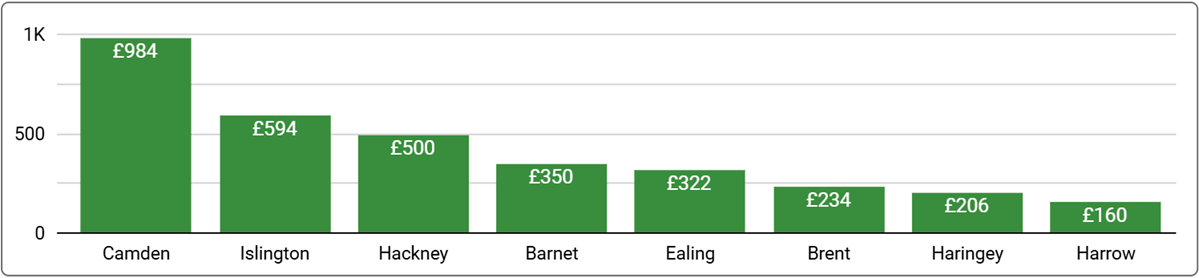

North London Shows Strong Rate Growth and Supply Expansion

North London bucked the regional trend with expanding supply in Q2 2025, with desk rates rising 4.0% quarterly to £390 while available space expanded 7.6% to 314,100 sq ft across 252 offices. The region's 11% annual rate growth suggests strong market development and what appears to be increasing business interest.

Supply expansion varied significantly across workspace categories. Traditional serviced offices maintained stable rates at £350 while space contracted 4.7% to 150,950 sq ft, suggesting healthy take-up. Customizable managed offices commanded premium positioning at £648 despite falling 15% in the past quarter, with space expanding 23%. The 80% annual expansion in managed offices likely reflects further landlord investment in flexible workspace solutions, though the rate decline may indicate pricing adjustments as supply increases.

Islington emerged as a notable region with rates increasing substantially to £594 (+49%), supported by exceptional annual availability to 155,450 sq ft across 105 offices, potentially establishing it as North London's premier destination. Hackney maintained market leadership at £500 across 51 offices, offering good Central London connectivity. Barnet demonstrated strong expansion with considerable annual space growth at competitive £350 rates, while Haringey provided exceptional value at £206 with growing inventory.

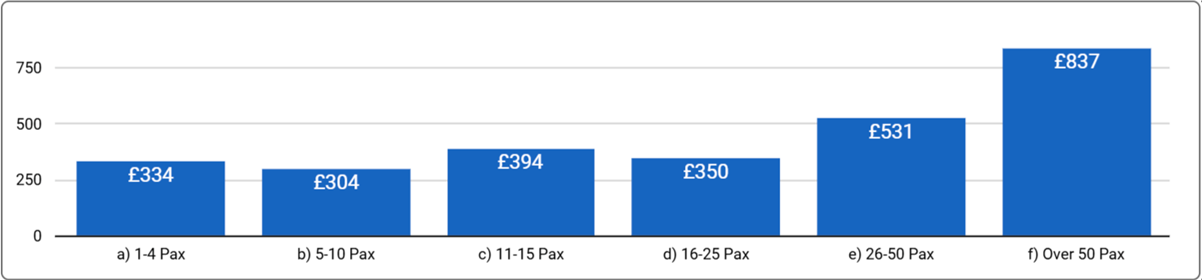

Larger businesses drove much of the region's expansion. Larger enterprise offices (50+ people) experienced a 20% quarterly increase in space with rates rising 3.8% to £837, while the mid-sized office segment (26-50 people) remained strong with rates climbing 4.7% to £531.

Source: Rubberdesk August 15, 2025

Navigation: Greater London | Central London | East London | West London | North London | South London

Get expert advice for your workspace needs today

We offer free, impartial comparisons of every serviced office across the UK, with full market coverage.

Or Call 0800 699 0655

Methodology

- All prices presented in this report are based on the median rate for a location or office size across an entire month

- Availability is based on the inventory inside the Rubberdesk platform and includes coworking desks and available offices (both serviced and managed offices) that hosts share with Rubberdesk

- Actual Flex office availability may be higher as not all hosts share 100% of their unoccupied office space with Rubberdesk

About Rubberdesk

Rubberdesk is the UK’s flexible office marketplace with thousands of fully furnished serviced offices and coworking desks ready for you to move in and rent by the month or year. Since having launched in the UK in early 2020, the Rubberdesk platform now encompasses over 7,00 offices, an estimated 7.9 million sq. ft. of space with a capacity for over 158,600 people.

Rubberdesk’s proprietary platform combined with industry insights from their office specialists helps customers find the best office for their unique needs. With a view across all available options, they simplify the process to create a bespoke shortlist, arrange tours and negotiate the best deals. All for free and without obligation.

Rubberdesk provides Flex Powered by Rubberdesk for commercial agents across the UK.

Rubberdesk also operates in Australia and Ireland.

Media Information

For further information, images and interview requests, please contact:

Laura O'Sullivan: +447456247744

Gareth Smith: +447762809786