UK Flexible Office Space Report - Q1, 2025

Rubberdesk's Flexible Office Space Report examines actual flex office availability, pricing and trends across London, Manchester, Birmingham, Leeds and Bristol.

See our Q3 2025 UK Flexible Office Market Report for our latest analysis of the UK flex space market.

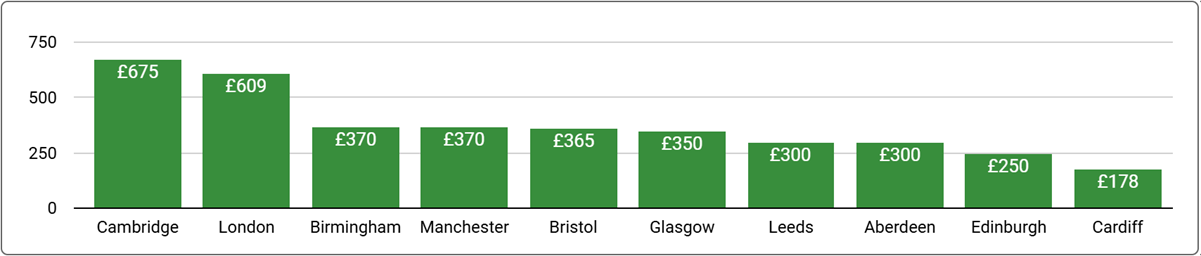

The size and structure of the UK Coworking and Serviced (Flex) Office can, in effect, be broken down to two separate markets 1) Greater London & 2) everything else. With London making up 75% of the available Flex Office space across the UK, it heavily skews the monthly rental rates & available space.

The following report looks at the cost and availability of flexible office space in key cities outside London. Please visit our Q2 2025 London Market Report for analysis of rates across Greater London.

UK Flex Space Expands Significantly in Q1 Amid Economic Headwinds

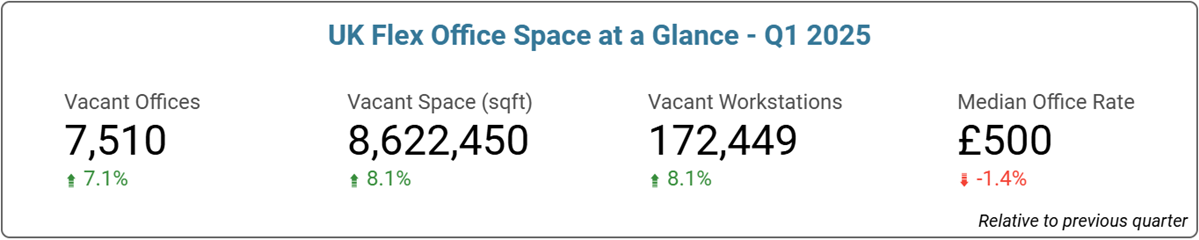

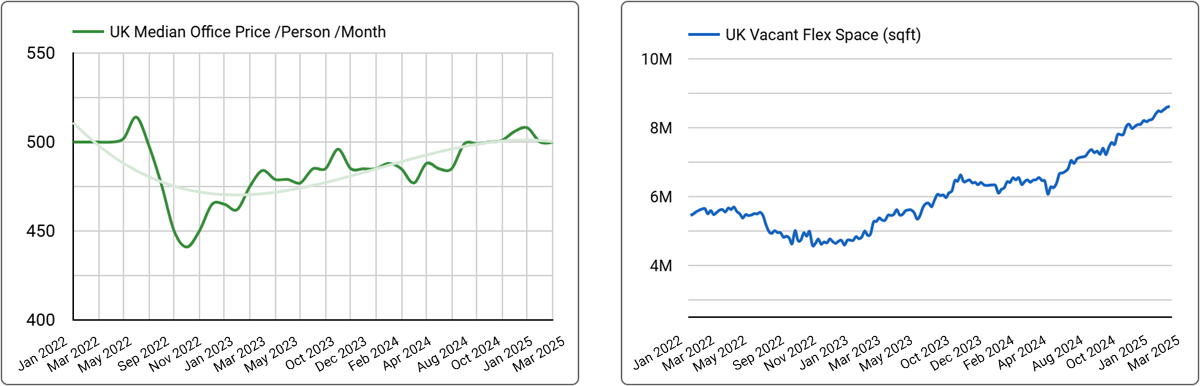

The UK flexible office market saw a significant increase in available space during Q1 2025, potentially reflecting cautious business sentiment and muted investment conditions in the broader economy.

Nationally, available space surged by 8.1% quarter-over-quarter (QoQ) and a substantial 31.6% year-over-year (YoY), reaching over 8.6 million sq ft. The increased supply led to a national median desk rate decrease of 1.2% QoQ to £500 per desk. However, reflecting persistent inflationary pressures and a resilient labour market with rising real wages, the national rate was up 2.2% YoY.

In addition to Greater London, this report delves into major markets beyond London to provide insight into trends across the UK.

London, dominating the market, saw desk rates remain stable QoQ (£625) but experienced a significant +7.7% QoQ and +39.0% YoY increase in available space.

Manchester (£379) saw modest rate growth (+1.1% QoQ, +5.3% YoY) alongside rising availability (+12.1% QoQ, +17.7% YoY).

Birmingham stood out with strong desk rate growth (+5.7% QoQ, +23.3% YoY to £370), contrasting with falling availability (-0.2% QoQ, -21.2% YoY).

Bristol rates were stable QoQ (£365) but availability decreased (-7.0% QoQ). Leeds (£322 per desk) saw a minor rate dip QoQ (-0.9%) despite a large space increase (+11.0% QoQ).

Leeds (£322 per desk) saw a minor rate dip QoQ (-0.9%) despite a large space increase (+11.0% QoQ).

Cardiff experienced a sharp rate decline (-11.0% QoQ, -20.9% YoY to £178) with stable availability. This regional divergence underscores the uneven economic landscape.

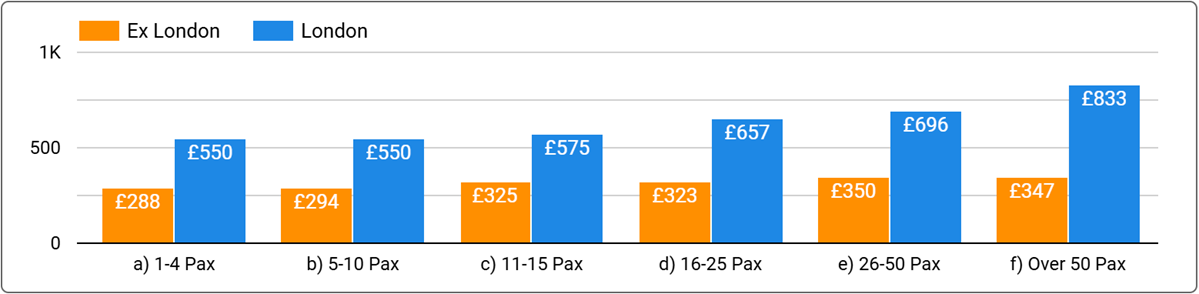

When it comes to comparing desk rates across the UK the following chart clearly shows how much the Greater London market skews the national median rate. A four person office in Greater London for example has a medium rate of £550 compared to £288 per desk across many other major cities. Alternatively, larger enterprise offices for teams of 50 or more staff cost £833 per desk in London compared to £347 per desk outside the city. It's this type of difference that clearly shows the benefits of a marketplace platform like Rubberdesk.

“The UK flexible office market experienced a notable expansion in Q1, with available space increasing nationally by 8.1%, contributing to slightly softer median desk rates, although this supply growth varied significantly across key regional cities.” said Tom Petryshen, VP Growth & Analytics at Rubberdesk.

Source: Rubberdesk April 2025

Managed Office Availability Soars 10.6% QoQ as Landlords Adapt to Market Shifts

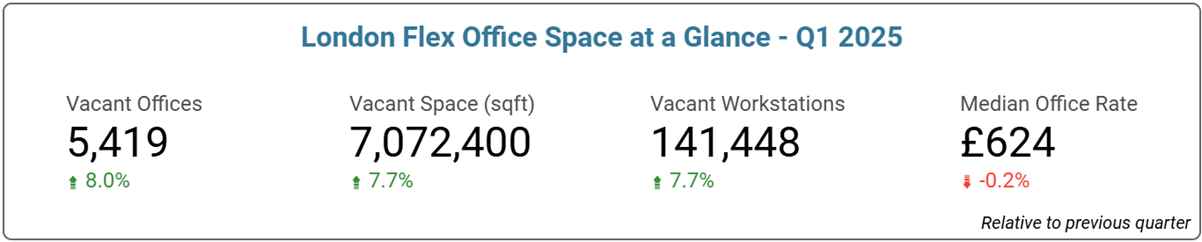

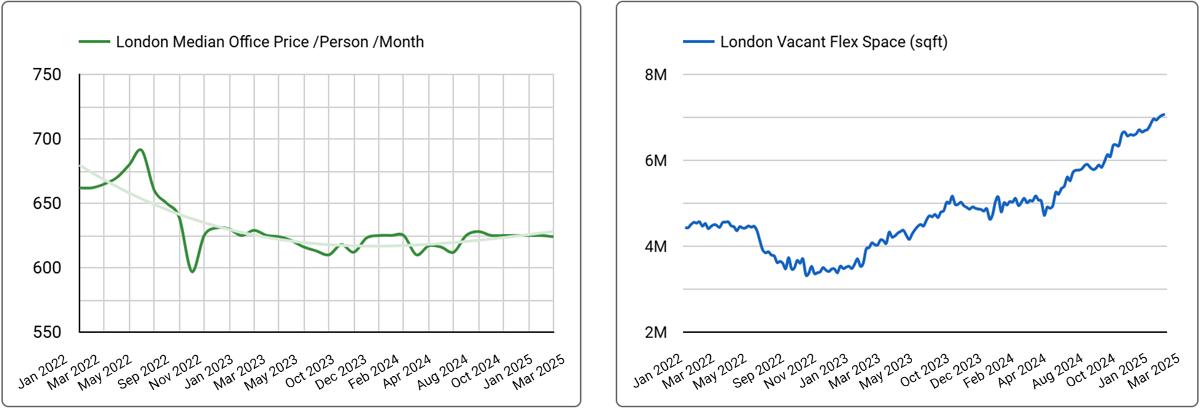

London's flexible office market saw overall average desk rates hold steady quarter-on-quarter at £625 per desk, even as available space grew significantly by 7.7% to over 7 million sq ft.

A key factor shaping market supply is the remarkable growth in Managed office space, expanding 10.6% QoQ and outpacing Serviced space growth (+6.1%). This surge, dramatically highlighted by a 111.0% YoY increase in Managed availability, reflects a dual dynamic.

Tenant demand for customised, private flexible solutions is strong, particularly from larger enterprises navigating economic uncertainty and hybrid work models.

Landlords are also actively contributing to this supply increase. Facing reduced demand for traditional 5-10 year leases, property owners are increasingly adopting managed solutions to meet evolving occupier needs and maintain occupancy.

Although Managed rates dipped slightly QoQ (-1.6% to £800), strong YoY growth (+10.7%) confirms the underlying appeal and value placed on this flexible model by both occupiers and landlords adapting to the market.

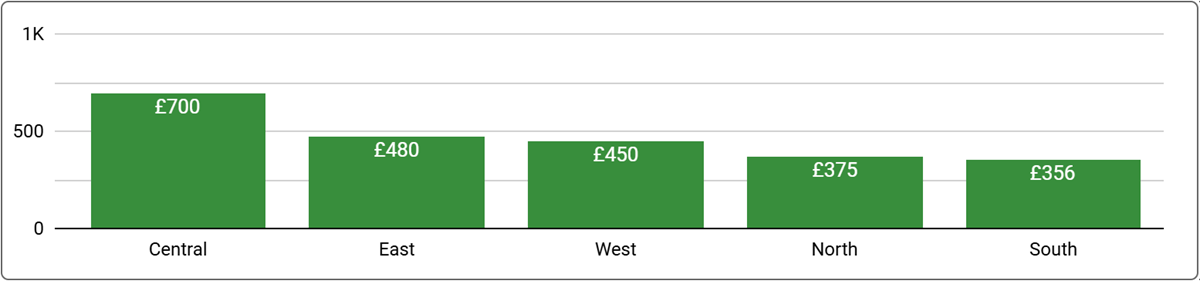

Regional performance varied. Central London saw the largest space increase (+27.1% QoQ) alongside a rate decrease (-6.5% to £700). Other areas like East and West London held rates steady QoQ despite space increases, while South London saw rates rise (+3.1%) with a large availability jump (+30.4%). This suggests the growing supply, particularly of Managed space, is reshaping market dynamics across the capital.

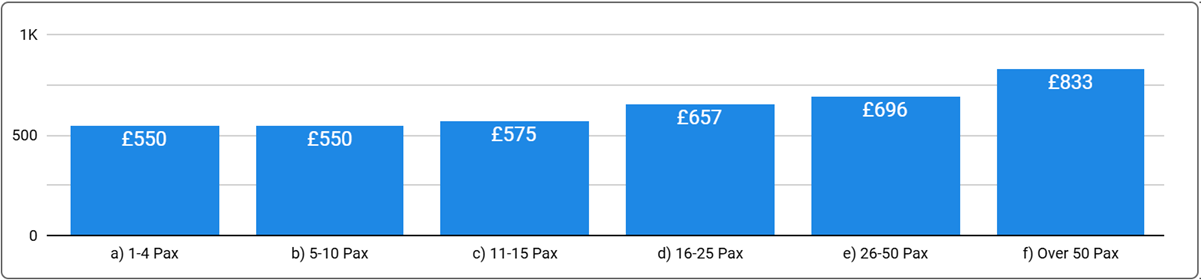

With 36% of the available flex office space catering to teams smaller than 10, this segment offers space across all areas of London at a median rate of £550 per desk while spaces for larger teams requiring more than 50 desks will cost ~£834 per desk due to the extra amenities and private breakout spaces.

Location also plays a role with enterprise offices in Central London in excess of £779 per desk for a Serviced Office and £936 per desk for a Managed Office.

Visit our Central London Office Price Guide and East London Office Price Guide for specific desk rates on regions within London.

Source: Rubberdesk April 2025

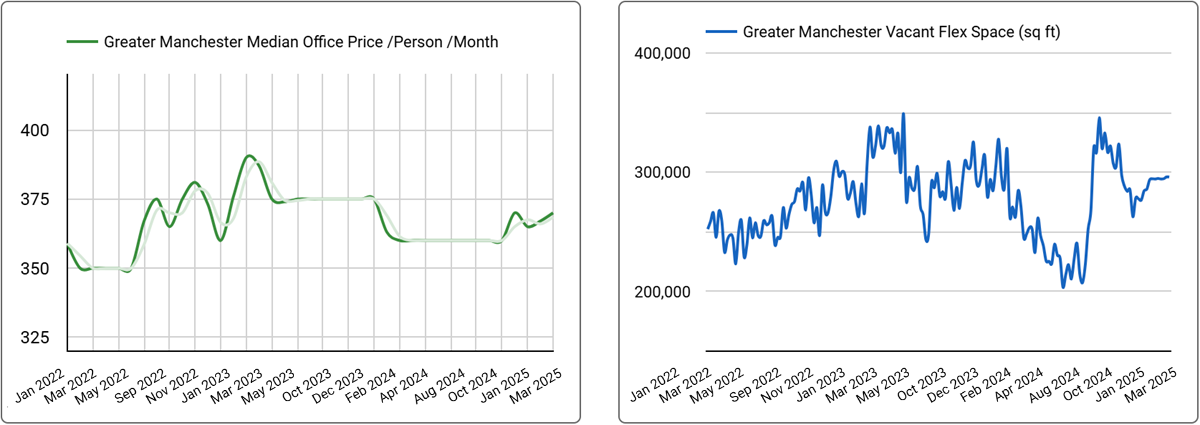

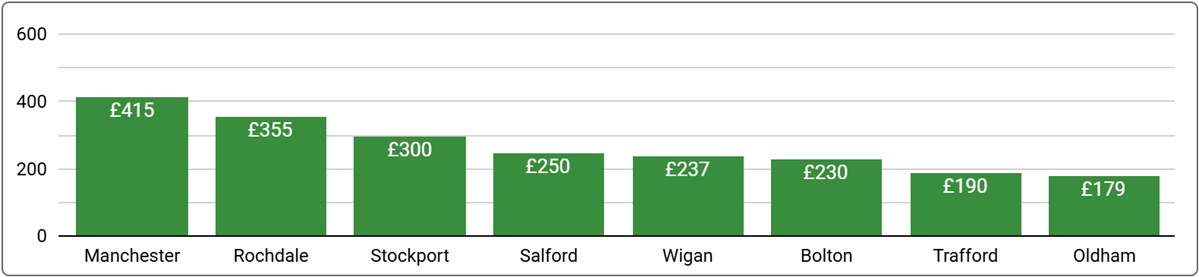

Resilient Manchester Sees Steady Rates, Expanding Supply in Q1

Greater Manchester's flexible office market displayed resilience in Q1 2025, with overall average desk rates holding steady quarter-on-quarter at £370 per desk, while available space expanded notably by 12.7% to 296,050 sq ft. This growth reflects Manchester's robust regional economy – the largest outside London – and its attractiveness due to lower operating costs and a vast talent pool, positioning it strongly despite broader UK economic uncertainties.

Manchester’s city-centre outperformed the wider region, with desk rates increasing (+3.8% to £415) alongside solid space growth (+9.3%). This suggests continued demand for prime city-centre locations. Performance in surrounding areas varied significantly: Salford saw rates hold steady (£250) but available space nearly doubled (+92.7%), indicating a potential supply surge. Trafford experienced a slight contraction in available space (-2.4%) with stable rates (£190). Other boroughs showed mixed results, highlighting diverse local dynamics.

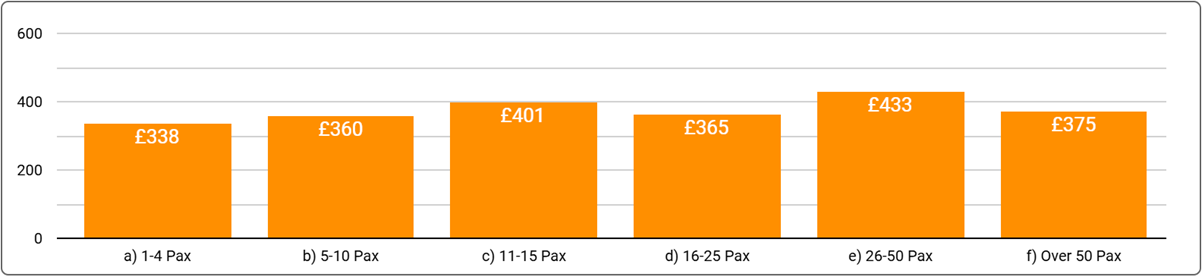

Pricing trends by size were varied. Smaller suites (1-4 desks) saw rates dip slightly (-3.4% to £338), while mid-size spaces (11-15 desks) saw an increase (+2.6% to £401). Rates for 16-25 desk spaces softened (-6.4%).

Availability grew across most size bands, particularly for larger requirements (26-50 pax space +17.8%; 50+ pax space +30.8%), suggesting a market adapting to accommodate bigger teams seeking flexible options.

Visit our Manchester Office Space Price Guide for more details on the Greater Manchester region.

Source: Rubberdesk April 2025

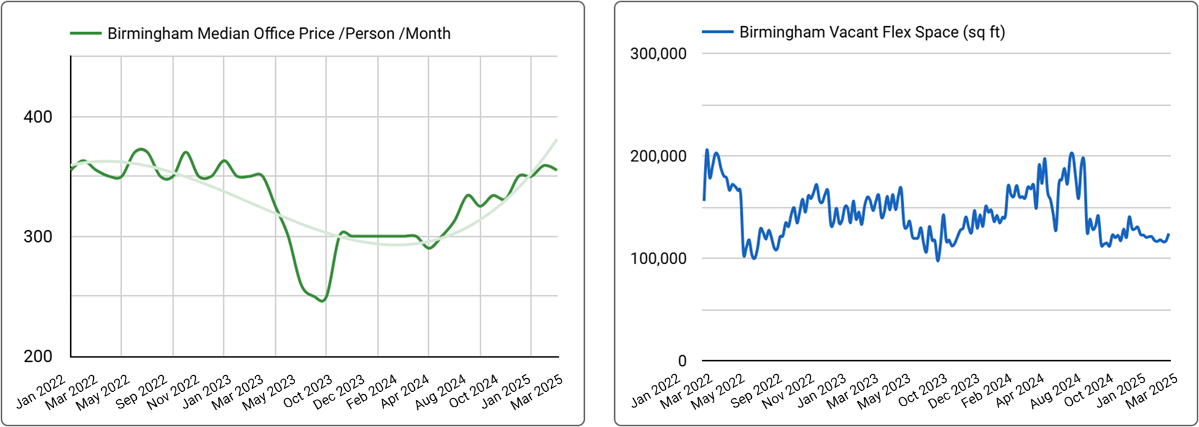

Birmingham Desk Rates Edge Up as Available Space Tightens

Birmingham's flexible office market experienced a tightening in Q1 2025, with the overall average desk rate nudging up 1.4% quarter-on-quarter to £355 per desk, while total available space contracted by 3.6% to 124,250 sq ft. This slight quarterly rate increase follows significant year-on-year price growth (+18.3%), occurring alongside a substantial reduction in available space compared to the previous year (-22.4%). This suggests resilient demand for the remaining space.

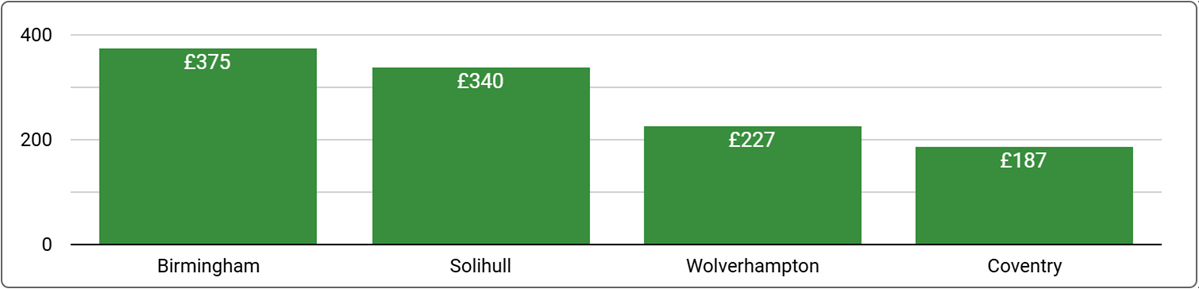

Birmingham city centre remained relatively stable QoQ, with desk rates up marginally (+0.8% to £375) and available space nearly unchanged (-0.2%). However, performance varied in surrounding areas; Solihull saw a significant quarterly drop in available space (-22.3%) with rates holding steady (£340). Wolverhampton saw a modest space increase (+9.4%), while Coventry experienced a small contraction (-4.9%).

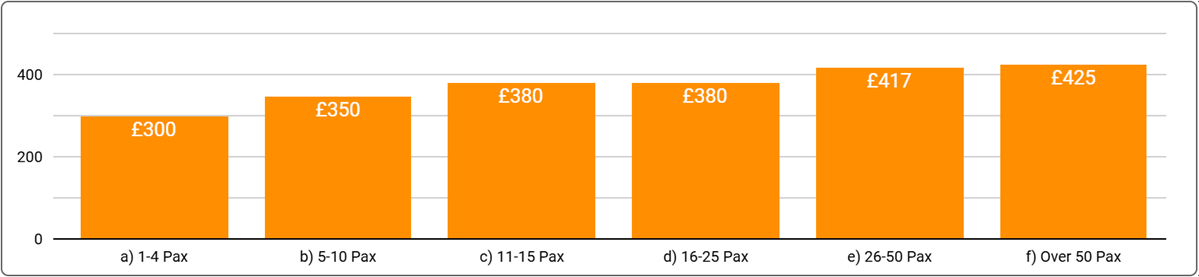

Pricing dynamics by office size were mixed. Rates for the smallest suites (1-4 desks) decreased (-7.7% to £300), while those for 5-10 desks jumped (+9.4% to £350). Mid-to-large category rates were stable or slightly increased QoQ, but this followed strong YoY growth. Available space tightened QoQ for most mid-large categories (11-50 desks), contrasting with growth in the smallest (1-10 desks) and largest (50+) segments.

This tightening supply, especially YoY, may reflect absorption driven by Birmingham's appeal to both established international firms and a growing startup scene.

Visit our Birmingham Office Space Price Guide for more details on the Greater Birmingham region.

Source: Rubberdesk April 2025

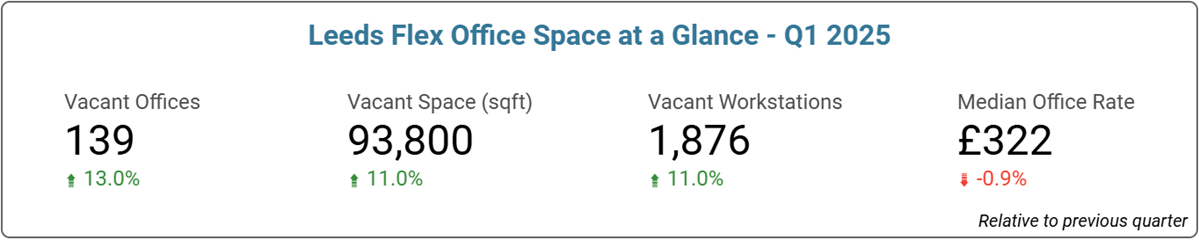

Leeds Q1 Flex: Space Grows 11% QoQ Amidst Rate Volatility

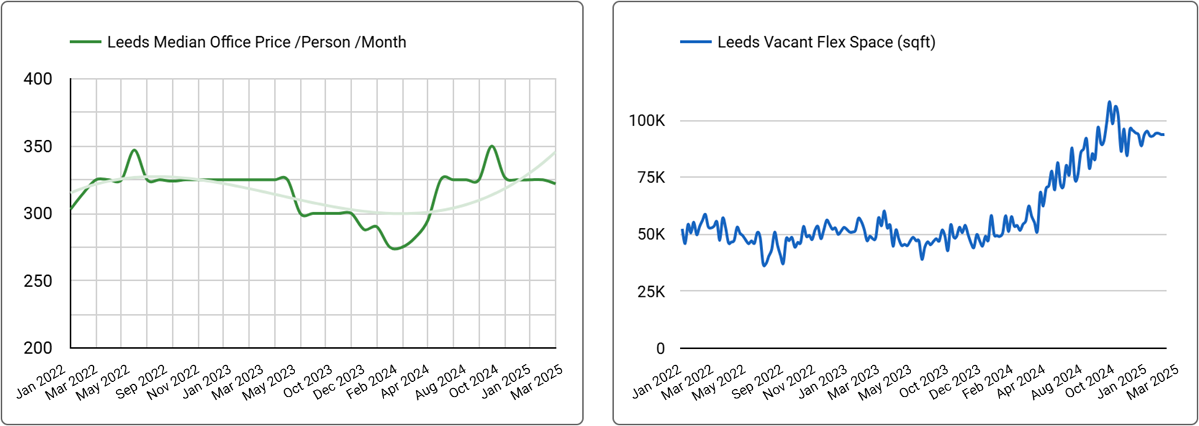

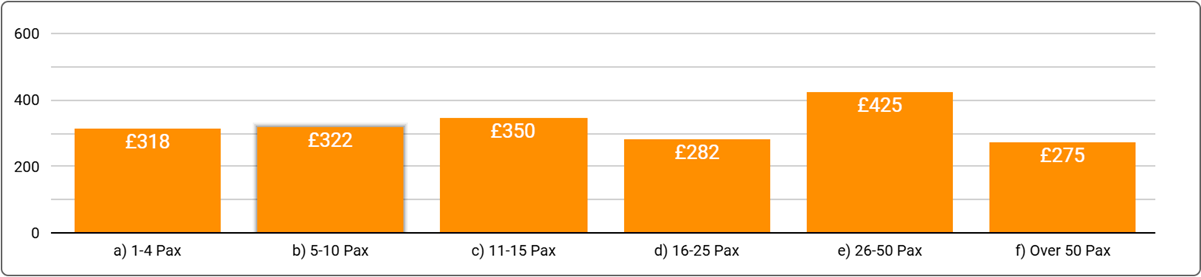

The Leeds flexible office market continued its expansion in Q1 2025, with available space increasing by 11.0% quarter-on-quarter to 93,800 sq ft. This quarterly growth builds upon a year of dramatic expansion, which saw total available space soar by 75.0% and average desk rates jump 17.1% year-on-year. The slight dip in average desk rates QoQ (-0.9% to £322 per desk) likely reflects this substantial increase in supply absorbing strong demand.

Growth was evident across most office sizes during the quarter. Available space increased significantly for nearly all categories, particularly for 16-25 desk (+32.4%) and 11-15 desk (+22.2%) requirements. Pricing by size showed volatility QoQ: rates for the smallest suites (1-4 desks) rose (+6.0% to £318), while notable decreases occurred for 5-10 desk (-8.0%) and 16-25 desk (-13.2%) spaces.

Conversely, rates for 26-50 desk offices jumped significantly (+30.8% to £425), following exceptional YoY growth (+70.7%) for this category.

Businesses will find spaces available from national operators including Workspace Hub, Citibase, Orega Serviced Offices, Regus and Landmark Spaces.

Find the perfect office in Leeds here.

Source: Rubberdesk April 2025

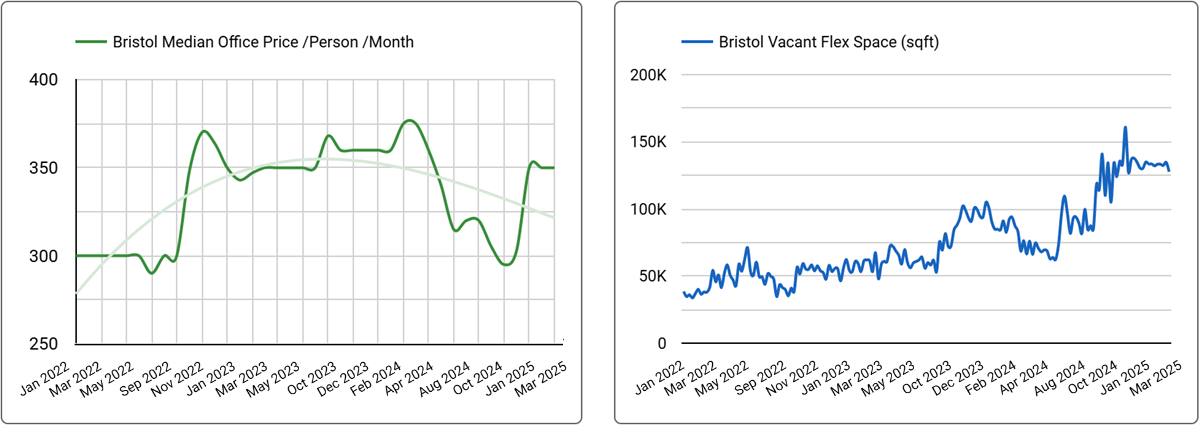

Bristol Q1 Flex Rates Surge 15.5% as Market Tightens

Bristol's flexible office market saw a dramatic shift in Q1 2025, with the average desk rate jumping significantly by 15.5% quarter-on-quarter to £350 per desk. This sharp increase occurred alongside a contraction in available space, which decreased by 6.7% QoQ to 127,700 sq ft. This dynamic likely reflects strong demand, potentially driven by Bristol's vibrant economy renowned for its creative, tech (as part of the "Silicon Corridor"), and aerospace sectors, absorbing the rapidly expanded supply seen over the previous year (space was up 53.6% YoY). This demand appears to be pushing up prices for the remaining space, even as broader UK economic uncertainty persists.

The quarterly trend contrasted with the year-on-year picture, which showed lower average rates (-6.7% YoY) but significantly more space (+53.6% YoY), suggesting recent market volatility and absorption.

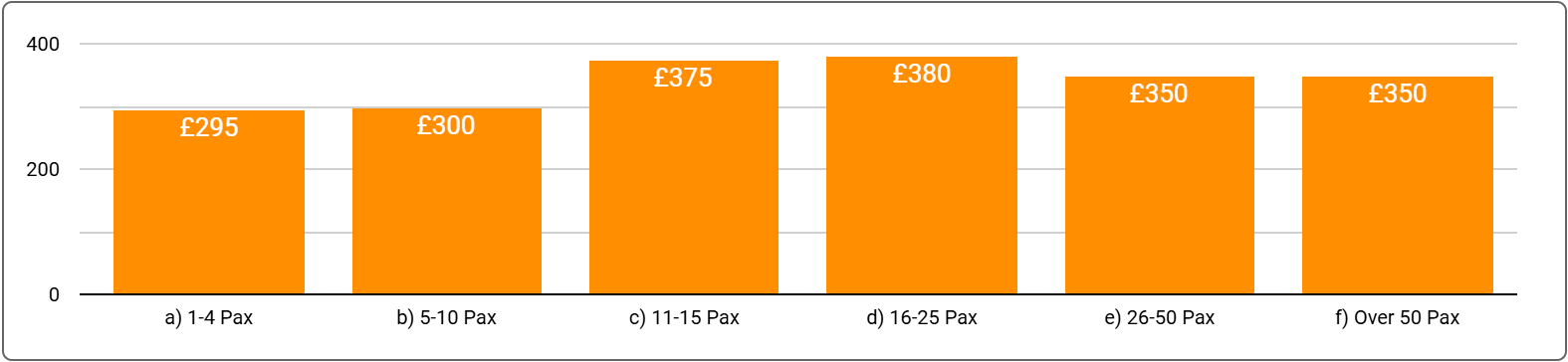

Pricing trends by size were notably mixed during Q1. While the overall rate surged, the smallest suites (1-4 desks) saw a sharp rate decrease (-15.0% to £295). Rates for larger suites (26-50 and 50+ desks) also softened QoQ (-6.7% and -12.5% respectively).

Available space tightened across most desk sizes, particularly for 11-15 desk (-31.4%) and 16-25 desk (-24.8%) requirements. This tightening supply, coupled with the overall rate jump, points towards strong competition for desirable spaces.

The top services operators include national players including Citibase, Chadwick Business Centre, Bizspace and Runway East.

Start your search for a private office in Bristol City today.

Source: Rubberdesk April 2025

Navigation: Summary | London | Manchester | Birmingham | Leeds | Bristol

Author: Tom Petryshen, VP Growth & Analytics

Get expert advice for your workspace needs today

We offer free, impartial comparisons of every serviced office across the UK, with full market coverage.

Or Call 0800 699 0655

Methodology

- All prices presented in this report are based on the median rate for a location or office size across an entire month

- Availability is based on the inventory inside the Rubberdesk platform and includes coworking desks, serviced offices, managed offices and subleased spaces that hosts share with Rubberdesk

- Actual Flex office availability may be higher as not all hosts share 100% of their unoccupied office space with Rubberdesk

About Rubberdesk

Rubberdesk is the UK’s flexible office marketplace with thousands of fully furnished serviced offices and coworking desks ready for you to move in and rent by the month or year. Since having launched in the UK in early 2020, the Rubberdesk platform now encompasses over 7,600 offices, an estimated 8.6 million sq. ft. of space with a capacity for 172,000 people.

Rubberdesk’s proprietary platform combined with industry insights from their office specialists helps customers find the best office for their unique needs. With a view across all available options, they simplify the process to create a bespoke shortlist, arrange tours and negotiate the best deals. All for free and without obligation.

Rubberdesk provides Flex Powered by Rubberdesk for commercial agents across the UK.

Rubberdesk also operates in Australia and Ireland.

Media Information

For further information, images and interview requests, please contact Laura O'Sullivan at Rubberdesk:

- E: [email protected]

- T: 0800 699 0655